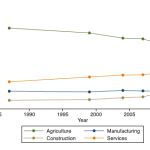

It is unfortunate that manufacturing is losing focus in India while all eyes are on so-called rapid growth of the services sector. Advertising and marketing campaigns have been peaking to impress consumers as well as investors while the manufacturing sector continues to struggle silently for growth. Barring in the areas of defence manufacturing and electronics, there are not many reports of new greenfield units coming up to expand the country’s manufacturing base. India’s so-called $1.2-trillion plan to snatch factories from China looks like a daydream. Investors — domestic and foreign — are not showing enough enthusiasm about deploying large sums in manufacturing despite its big growth potential in the world’s most populous country. In India, manufacturing accounts for 78 percent of total industrial output. Logically, the country’s economic growth should be linked with its manufacturing growth. But, it is not happening to the extent it must.

In this context, the latest observation of External Affairs Minister Subrahmanyam Jaishankar is quite strong and meaningful. Last week, the minister said: “I think we should stop looking for a China fix. If we are really to sustain and take the economy to a different level, we have to create a kind of domestic vendor chain that a serious manufacturing economy will do….. There is no major country in the world which has sustained or enhanced its global position without some commensurate build up of manufacturing. I have always believed that this focus on services was actually an elegant excuse for being incompetent in manufacturing…… In the name of opening the economy and globalisation we should not end up de-industrialising this country. We should not allow level playing fields in this country for others to subside their rich. That is economic suicide. We need to be clear that every country must support its manufacturers, and must support its businesses. We must not allow other businesses to enjoy advantages in our country at the expense of others.”

Few ministers in the government — present or past — have made such a bold assessment of the situation and pressed for action to put manufacturing at the top of the country’s industrial and business agenda. In the last 10 years, India did not see even a major manufacturing IPO (initial public offering) entering the market to raise funds from the public for expansion, diversification and growth. The big IPOs came mostly in the services sector and shared by both state-controlled and private enterprises. Many of such enterprises failed to keep the promises to investors made in their offer documents.

Take for instance the mega IPOs that hit the market in the last five years or so. Not one came from a manufacturing enterprise. Such IPOs included LIC of India (Rs.21,000 crore), Paytm (RS.18,300 cr.), GIC (Rs.11,256.83 cr.), SBI Cards (Rs.10,354.8 cr.), New India Assurance (Rs.9,485.82 cr.), Zomato (Rs.9,375 cr.) and HDFC Standard Life (Rs.8,695.01 cr.). Stocks which are selling at below their issue prices in recent times are: Inox Green Energy, Keystone Realtors, Dharmaj Crop Guard, Uniparts India, Abans Holdings, KFin Technologies, Elin Electronics and Radiant Cash Management Services.

The successive governments found it tough to attract foreign companies to invest large in the country to beef up its manufacturing sector since the economic reforms were initiated three decades ago. The current government’s Production Linked Incentive (PLI) Scheme is yet to generate enough response from large investors in manufacturing. Investments in India’s manufacturing sector have hardly been a priority of foreign investors despite the fact that the country’s investment regime is now among the most liberal among all major economies. The manufacturing sector has been attracting less than a fourth of the total foreign investment in recent years. The PLI scheme has not changed this pattern. The published data for April to December of 2022–23 showed that the manufacturing sector had attracted less than 21.7 percent of the total FDI inflows. On the contrary, foreign investors find India’s service sector very attractive, investing several times more in this sector compared to manufacturing. During April-December 2022–2023, FDI inflows into the service sector were 74.6 percent of the total.

India’s slow growth in the infrastructure sector, delays in land acquisition for large manufacturing projects and various political pressures on the government on project location have failed several large manufacturing projects in the country. There is little to justify the delays in implementation of the government’s own mega infrastructure projects involving roadways and highways, the railways, and waterways. In the road transport and highways sector, 407 out of 717 projects are delayed. For railways, out of 173 projects, 114 are delayed, while in the petroleum sector, 86 out of 146 projects are running behind schedule.

The government’s Infrastructure and Project Monitoring Division (IPMD) is mandated to monitor central sector infrastructure projects costing Rs.150 crore and above based on the information provided on the Online Computerised Monitoring System (OCMS) by the project implementing agencies. Among the IPMD-monitored major projects running behind schedule is a 1,350 km-long Delhi-Mumbai Expressway at an expected cost of over Rs. 1,00,000 crore. Over 240 projects reported time and cost overruns. Together, they bring direct or indirect impact on new manufacturing ventures linked with these new infrastructure connects.

Finally, the manufacturing sector needs new local entrepreneurs and long-term stayers. Unfortunately, this is not happening. India has not seen many manufacturing enterprises such as Larsen and Toubro (L&T) coming up in the last 70 years. Most of India’s valued engineering manufacturing and production enterprises are several decades old. Younger entrepreneurs are more interested in startups, easy money, high valuation and quick exit. In 2021, India was creating unicorns almost every week. Funds and investors were chasing founders across sectors, driving up valuations and creating billion-dollar companies. As many as 44 unicorns were created in 2021, with a total valuation of $93 billion, as per Invest India data.

India is home to 100 unicorns with a total valuation of over $300 billion. In contrast, India’s old manufacturing companies are growing at their own pace, between four and five percent. The country’s biggest manufacturing segments are: basic metals (13 percent of total production); coke and refined petroleum products (12 percent); chemicals and chemical products (8 percent); food products (5 percent); pharmaceuticals, medicinal chemical and botanical products (5 percent); motor vehicles, trailers and semi-trailers (5 percent); machinery and equipment (5 percent); other non-metallic mineral products (4 percent); and textiles, electrical equipment and fabricated metal products (3 percent each). Time looks tough for India’s future manufacturing growth. Maybe, the government itself should take the initiative as China did in the last three decades. (IPA Service)

The post Time Looks Tough For India’s Manufacturing-Led Growth first appeared on IPA Newspack.

Follow Arabian Post

Select Arabian Post as your preferred source on Google and MSN News for trusted business news and Arab politics and updates.